Business expectations rise unexpectedly

Commentary on the Logistics Indicator Q3 2025 by Kai Althoff, Chairman of the Board of Bundesvereinigung Logistik (BVL) e.V. and CEO 4flow SE

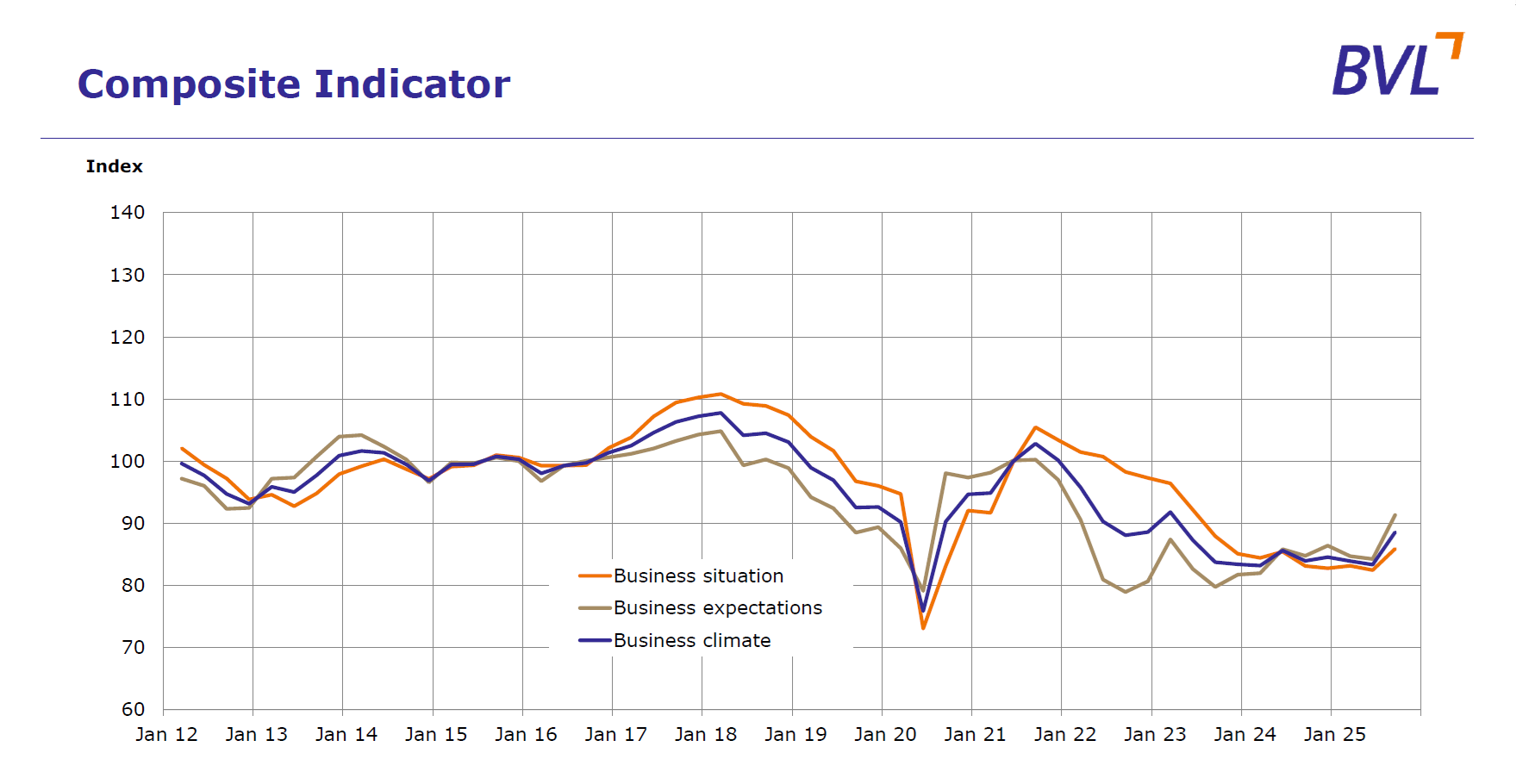

The figures from the BVL and ifo Institute's logistics indicator for the third quarter of 2025 come as a surprise in light of the negative reports on economic development and unemployment figures: Business expectations in the logistics sector have jumped significantly and are now at their highest level since the end of 2021. The indicator rose from 84.2 in the previous quarter to 91.3. The highest rating was achieved by shippers with 92.9, which corresponds to an increase of 4.8 points and is the best value since Q1/2022. The biggest improvement, at +7.9, is among logistics service providers, who reached 89.2 – the best value since Q4/2021. There have also been improvements in the current business situation and business climate – the latter reached 88.6, the best value since the first quarter of 2022, while the business situation reached 85.9, the best value in two years. Of course, all this should not obscure the fact that we are still below the normal value of 100 in all areas, i.e., at a very low level. Nevertheless, the significant improvements are noteworthy.

How can this be explained? On the one hand, economic stimulus programs are playing a role: it is assumed that the government packages will trigger investments that have been held back for a long time. In addition, companies have announced plans to invest €630 billion to strengthen Germany as a business location. Even though this includes not only new announcements but also many projects that have already been approved, the scale of corporate investment is nevertheless positive. A second point could perhaps be described as “recovery through reassurance.” The conclusion of customs agreements has brought at least a little planning security. Even though Europe, and with it Germany as the largest economy and leading export nation, is at a disadvantage compared to the previous framework conditions, it is now at least clearer what can be expected. But there are also signs of slight easing among companies in real terms: since the spring, the current situation has improved month by month for both shippers and logistics service providers – in August, it broke through the 90 indicator value again for the first time among service providers.

A look at the various sectors in industry and trade reveals a very mixed picture. The automotive industry is under enormous competitive and cost pressure. The worst-case scenarios were avoided in the customs negotiations. There have been more positive developments recently in the metal and electrical industries and in residential construction. The mood in the security and defense sector remains optimistic. The mechanical engineering sector is currently still rather skeptical about the current year, with an upturn not expected until 2026 at the earliest. The mood in the chemical industry remains negative, and consumers are still pessimistic, as the HDE consumer barometer shows. In this respect, no trend reversal can be deduced for logistics either.

The positive developments can therefore be explained by a pronounced bottoming out. The current situation is priced into the value chains. The question now is whether a positive trend can emerge. This is likely to be the case.

I am curious to see the mood that awaits me at the end of October at the BVL Supply Chain CX in Berlin, where we will have representatives from the entire economic sector in one place and can experience live how the industry is doing—and, above all, how innovatively and forward-looking it is dealing with topics such as AI, sustainability, and demographic change.

Downloads

- Detailed results ( PDF, 127 Kb)

- Commentary by BVL's President Kai Althoff ( PDF, 63 Kb)

- Commentary by ifo Institute, Prof. Wollmershäuser ( PDF, 58 Kb)