Situation deteriorates

Commentary on the Logistics Indicator Q2 2024 by Prof. Timo Wollmershäuser, ifo Institute

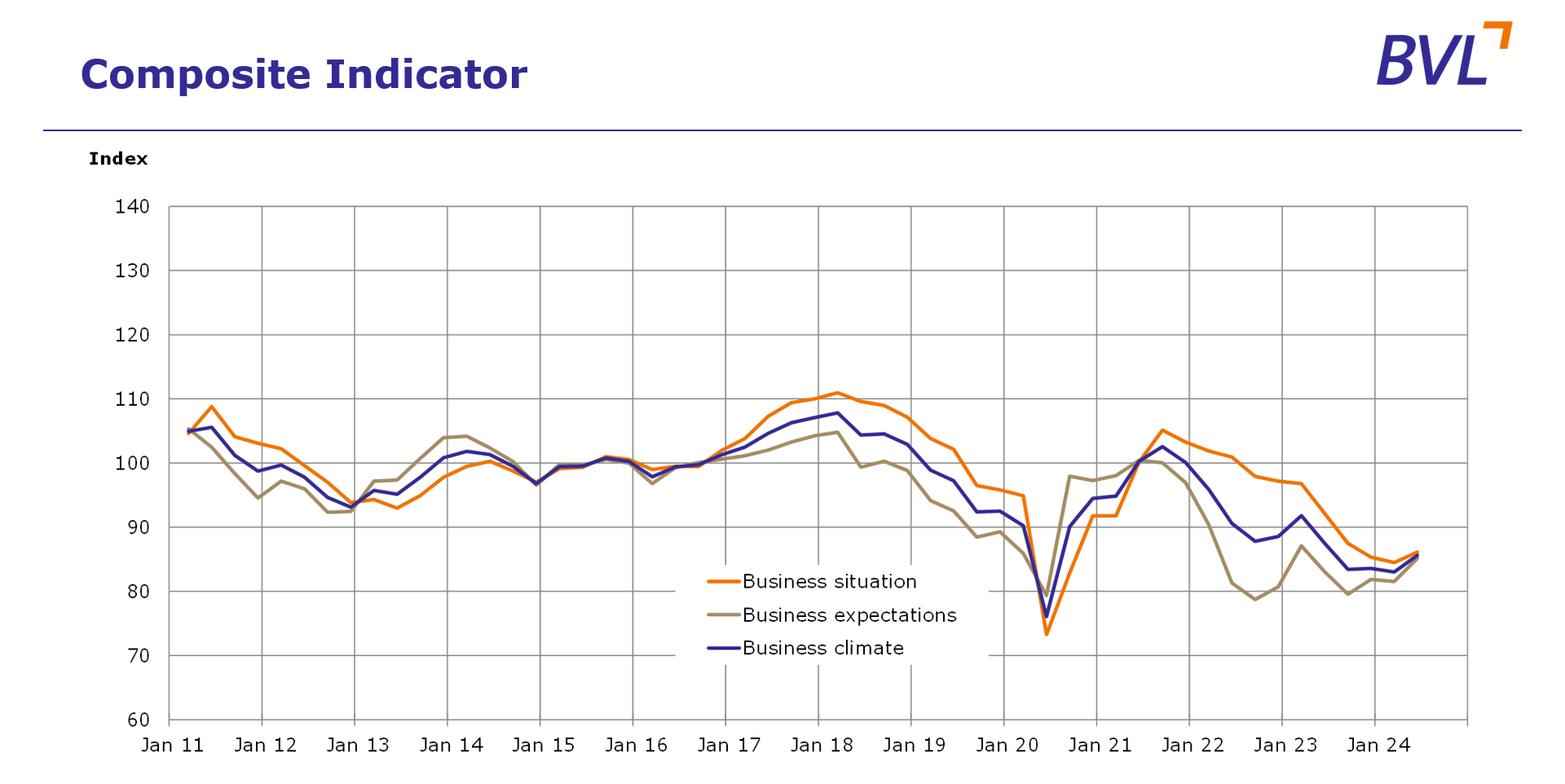

The business climate in the logistics sector in German deteriorated again in the third quarter of the year after improving in the previous quarter. The corresponding index fell from 85.3 points to 84.4 points, according to the monthly surveys of the Logistics Indicator, conducted by the ifo Institute on behalf of the BVL – The Supply Chain Network (BVL) as part of its economic surveys. The business situation also suffered a setback and was worse than in the previous quarter. The participants were therefore widely dissatisfied with their business situation. The expectations indicator indicator also fell - companies in the logistics industry were therefore pessimistic about the coming six months.

The business climate for logistics service providers also deteriorated again following the significant improvement in the previous quarter. The climate indicator fell from 84.1 index points to 82.6. Service providers assessed both their business situation (83.3 currently, 84.7 most recently) and their business expectations (81.9 currently, 83.4 most recently) worse than in the previous quarter. The companies did not expect their business situation to improve in the coming six months. Declining demand was widely reported - and thus significantly more frequently than in the previous quarter. In terms of demand expectations, however, the negative voices outweighed only slightly. Order backlogs fell again significantly compared to the previous quarter. Participants were very widely dissatisfied with their order backlogs. The last time they were even more dissatisfied was in the third quarter of 2020. However, job cuts in the next three months were only planned selectively.

Companies from trade and industry reported a situation that was even less favorable than in the previous quarter. At the same time, business expectations improved slightly. As the downward trend in the business situation prevailed, the business climate was once again less favorable. The main indicator stood at 86.1 index points, compared to 86.8 recently. Inventories remained unchanged. In contrast to the previous quarter, prices are set to rise again. In addition, employment plans remained restrictive.

The German economy is stuck in crisis. There has been no revival in economic output for more than two years. The crisis is primarily a structural crisis. Decarbonization, digitalization, demographic change, the coronavirus pandemic, the energy price shock and China's changing role in the global economy are putting established business models under pressure and are forcing companies to adapt their production structures. There is much to suggest that these adjustment processes are not yet complete. The long-term effects will probably only be able to be assessed in retrospect in a few years' time. The slump in investment and productivity in recent years has led, at least temporarily, to a significant downward revision of production potential. The weak private investment activity is likely to be a consequence of business closures, production shutdowns and relocations as well as the high level of economic policy uncertainty. The productivity standstill is accompanied by shifts in employment growth from the industrial to the services sector, which also took place in the course of demographic change.

However, the crisis is also a cyclical crisis. Utilization of existing production capacity has been falling for more than two years and underutilization has recently increased noticeably again. According to the ifo economic surveys, companies in all of the economic sectors are complaining about persistently weak demand. In the construction and manufacturing industry, the order backlogs of previous years have melted away, and a turnaround in new orders is still not in sight. The consumer-related sectors hardly benefit from the strong real wage increases and the associated gains in purchasing power. On the contrary, private households are holding back on spending and are setting aside an increasing proportion of their income as savings.

The leading indicators currently available do not suggest an economic turnaround for the third quarter of 2024. In August, the ifo business climate deteriorated for the third for the third time in a row and the order situation in all economic sectors is still assessed as poor. A gradual recovery is not expected until next year. Nevertheless, incoming orders in the construction and manufacturing sectors have recently not fallen any further. The export business is supported by the global economic development which is likely to maintain its current momentum. The construction sector is being driven primarily by public construction. Residential construction is likely to stagnate for the time being, as newly built residential properties have hardly become more affordable. As wages will continue to rise significantly higher than prices in the coming quarters, purchasing power will continue to return. Thus consumer spending should also recover. All in all, the price-adjusted gross domestic product after a decline of 0.3% last year will probably only stagnate this year. A gradual recovery is likely to set in over the next two years, in the course of which economic output will increase by 0.9% and 1.5% respectively.

Downloads

- Detailed results ( PDF, 948 Kb)

- Commentary by ifo Institute, Prof. Wollmershäuser ( PDF, 79 Kb)